In normal markets, when demand drives prices up, suppliers will produce more to meet the demand and take advantage of the higher prices. That’s how the oil market is supposed to work.

But the Biden administration has taken a number of steps to hamper oil investment, by:

- telling drillers and producers of oil that they will be bound by ever-more-restrictive climate change rules

- eliminating pipeline approvals

- and preventing new drilling on federal lands

Those actions have given power back to OPEC, which has no incentive to produce more oil, and even said it won’t yesterday.

Add on top of Biden’s anti-oil measures the modern-day Salem witch hunt that is the EGO-driven development of ESG funds, and is it any wonder gasoline prices are rising so fast?

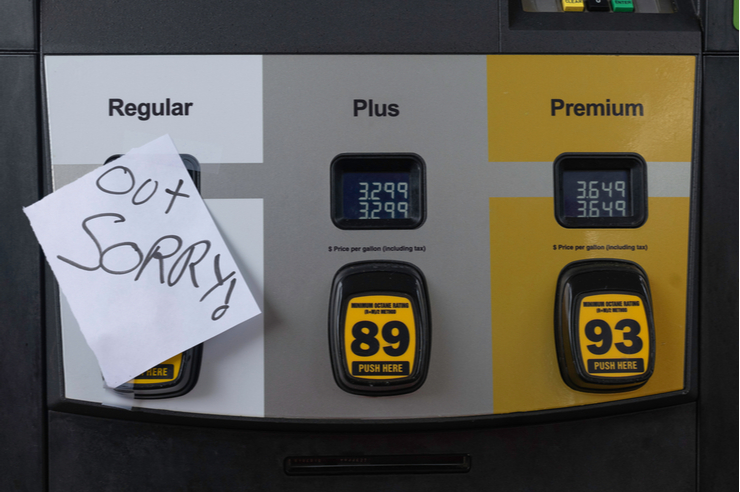

Gas prices rose to the highest levels since 2014, amid increased demand and concerns about supply.

According to AAA, the national average for a gallon of regular unleaded gasoline rose two cents to $3.204, the highest level it has been since October 2014, according to USA Today. California’s prices are the highest, at an average of $4.414 per gallon. Mississippi has the lowest prices, averaging $2.829 per gallon.

Gas prices have also risen more than a full dollar since last year, from $2.186 in October 2020.

The highest recorded national average was $4.114, in July of 2008.

The increase in prices at the pump is likely due to the substantial increase in oil prices. Crude oil prices have spiked to more than $80 per barrel, according to Bloomberg.

Action Line: It appears that the Biden administration will be defined by shortages and inflation. Protect yourself from shortages and inflation by preparing both your household and your portfolio ahead of time. If you’re serious about beating inertia and getting ahead of Bidenomics, click here to sign up for my free monthly Survive & Thrive newsletter. I’ll help you defeat inertia and make a positive impact on your life, and the life of your family. But only if you’re serious.